The mass affluent investor segment has been underserved by traditional wealth managers and retail banks, with business models geared towards the mass market or high-net-worth customer segments. This market gap has spurred growth of new fintechs with low-cost digital-direct business models and has driven substantial investments into digital platforms by established institutions.

The mass affluent market represents a dynamic and diverse group of approximately 32 million individuals who – with investable assets ranging from $100,000 to $1 million – fall between traditional mass-market retail banking and high-net-worth provision.

While mass affluent needs may not be as complex as those of their wealthier counterparts, these customers’ financial aspirations extend beyond basic savings accounts and they are demanding more sophisticated solutions and an increasingly personalized, ‘high touch’ experience.

The mass affluent market stands as an attractive prospect for banks and wealth managers, given their desire to combine their banking and wealth strategies. Although the mass affluent are more price sensitive to paying for advice, their penchant for digital tools presents opportunities for innovative sales and service approaches.

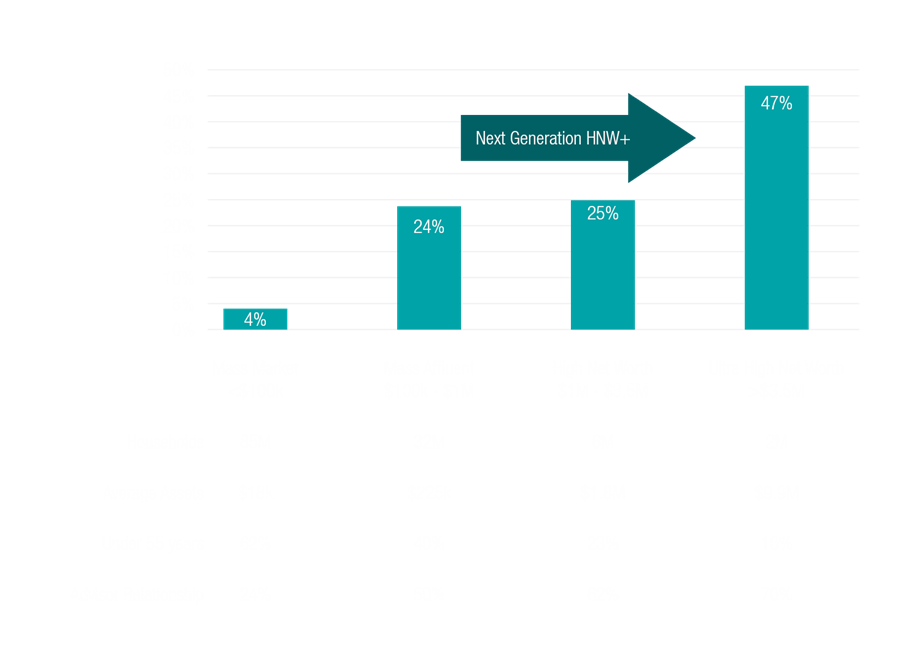

Moreover, with above-average incomes, a higher risk appetite, and a propensity to invest heavily in growth-focused investments, this market likely possesses the potential for more sophisticated financial planning and tax strategies as they build wealth in the future. Financial institutions that successfully cater to this segment stand to reap long-term rewards due to the ‘great wealth transfer’, with trillions of dollars in assets set to be handed down from baby boomers to their heirs over the next 20-plus years.

Shifting from a Single to an Omnichannel Model

Offering an integrated and consistent experience that meets customer’s needs across the sales lifecycle, an omnichannel business model also allows providers to cross-sell advice, leverage client relationships, see into customer data across multiple acquisition channels, and deliver product offerings and service models in a highly coordinated fashion.

Source: Capco

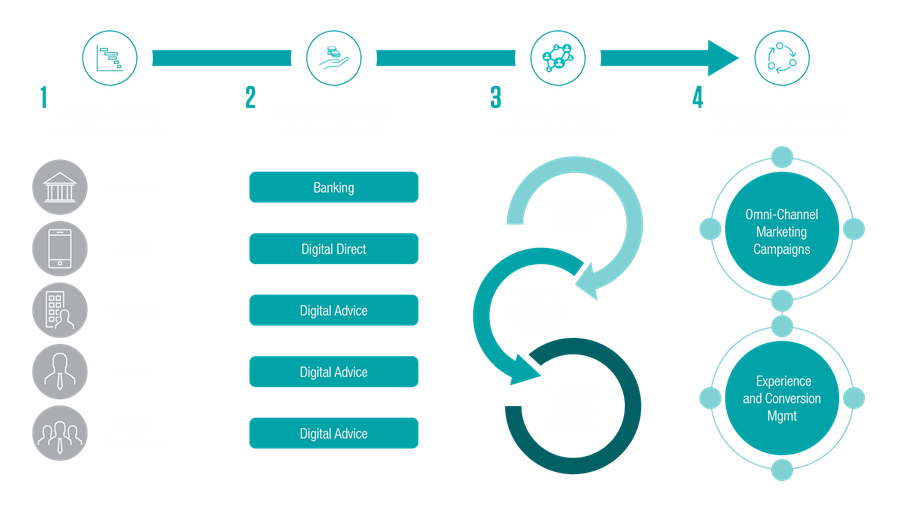

Omnichannel Business Model

There are four distinct characteristics of well-executed omnichannel models

- Multiple customer acquisition channels: Retail banking, digital brokerage, digital advice, workplace stock and retirement plans, and remote or personal advisors are key customer acquisition channels depending on what life stage customers are in and their corresponding needs. Synergies will be unlocked through the combination of channels and by offering the right products and services to the right customers at the right time.

- Differentiated product offerings and service models: Omnichannel wealth managers differentiate both the product offerings and service models to seek unique and compelling value propositions for each segment and persona. They also optimize the cost-to-serve across different service models, including digital-direct, remote advisors, and varying levels of advisor team support.

- Enhanced cross-selling and migration platform: As customers’ needs evolve, omnichannel wealth managers migrate customers towards higher value advice models. A cross-selling and migration platform has both a push and pull component, meaning the push will be enabled by data analytics-driven personalized content and calls-to-action, as well as structured referral programs across the channels. The pull is created through educational content, research, and loyalty or rewards programs that incentivize balance sheet consolidation. Typically, prospecting effectiveness is significantly higher in cross-sell situations where established awareness and relationships are present. Human referrals are also a very effective growth engine. Overall, successful strategies incorporate both digital and human interaction.

- Continuous experience and conversion optimization: Wealth managers must stay very close to their clients to design the ideal product, market fit, and go-to-market (GTM) approach. The most successful strategies will be based on continuous optimization of products, experiences, sales, and marketing. Additionally, data-driven feedback loops will help to optimize performance over time, though they require effective collaboration across multiple functions, including marketing, sales, platforms, products, and field organizations.

Tailoring Products and Services

Capturing the mass affluent market requires a dynamic approach to tailoring products and services since these customers are not a homogenous group, and the more an institution can customize its solutions, the more the institution will be able to attract and retain this client group.

- Building Relationship and Personalization: Unlike generalized services offered to the broader retail market, the mass affluent segment demands personalized attention. Banks and wealth management firms should take the opportunity to develop deeper relationships by understanding each client's financial goals and tailoring their services accordingly. A digital-hybrid approach enables bankers and financial advisors to gather insights through online interactions and utilize them for more meaningful in-person conversations.

- Enhancing Accessibility and Convenience: Mass affluent customers, like most of the modern population, expect easy access to their financial information. Online platforms provide a secure space for clients to track investments, review financial plans, and execute transactions at their convenience. Financial institutions need to capitalize on both online and offline interactions to enhance customer satisfaction and build loyalty.

- Navigating Complexity: Since many individuals in this segment are business owners, professionals, or investors—often with a variety of income sources and investment portfolios—the mass affluent have multifaceted financial needs. A digital-hybrid approach enables financial institutions to offer robust investment tools, retirement planning, tax optimization strategies, and estate-planning solutions. The online component allows clients to explore these options at their own pace before engaging in detailed discussions with advisors.

- Building Trust Through Technology: One of the key challenges in the financial sector is building and maintaining trust. The digital-hybrid strategy can help by offering transparent communication and secure technology. Cybersecurity measures and encrypted communication channels provide peace of mind to clients, ensuring that their financial data and sensitive information are well-protected.

Conclusion

The mass affluent market is a unique and underserved segment that provides distinct opportunities for banks and wealth managers seeking sustained growth. The ability to align resources to attract and retain mass affluent customers with a compelling offering may be challenging, but equally rewarding over time.