The UK’s Consumer Duty came into force on July 31, placing a significant burden on financial services firms to set higher and clearer standards of consumer protection, put their customers’ needs first and demonstrate compliance with both imperatives.

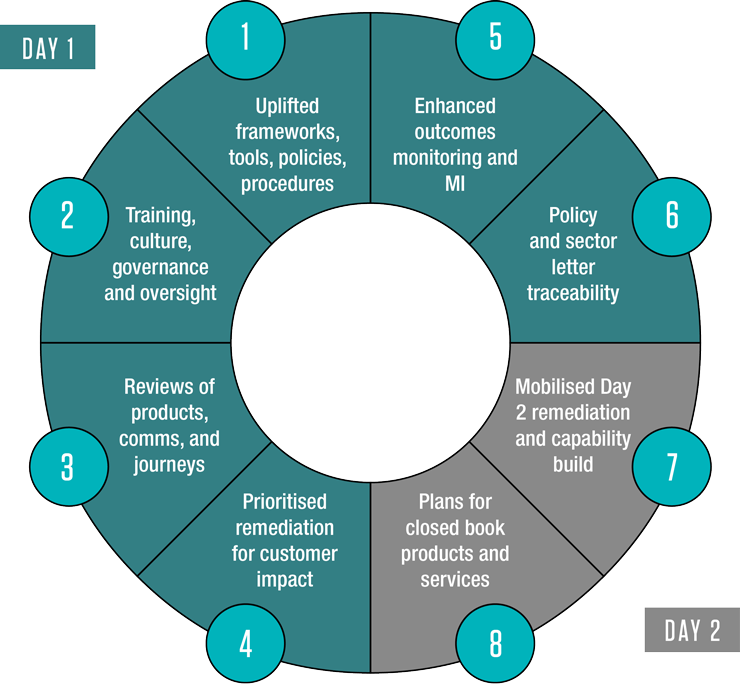

Below we explore eight key areas of focus for firms as they pivot from Day One preparations to assessing their relative maturity and ability to meet their obligations under Principle 12 of the Duty.

1. Uplifted Frameworks, Tools, Policies and Procedures

Firms should be able to demonstrate that their key frameworks have been – and continue to be – reviewed and uplifted. We would expect this to be reflected in product governance operating models, conduct frameworks, pricing and interest rate setting strategies, vulnerability frameworks, third-party risk frameworks under the Senior Managers & Certification Regime, and second and third line of defence policies, as well as processes and procedures for critical journeys. If all this can be evidenced, then firms will be able to demonstrate going forward that the rules have been fully met.

2. Training, Culture, Governance and Oversight

A consistent theme from the Financial Conduct Authority (FCA) has been cultural change and learning. Firms should be able to demonstrate that a comprehensive training programme has been delivered that goes beyond ‘one size fits all’ e-learning and clearly breaks down the desired behaviours that firms want to see and measure for various roles. A focus will naturally be on customer facing roles – however, it is equally important that firms can demonstrate how governance decisions consider customer outcomes.

3. Reviews of Products, Communications and Journeys

Most firms have structured their implementation programmes using a sequential ‘review, triage and remediate’ methodology. It is critical that firms can evidence how the review activity was completed, quality assured and documented. In particular, firms must demonstrate that, where no changes have been made to products, communications or journeys, these decisions are predicated on the outcome of a thorough review.

4. Prioritised Remediation for Customer Impact

Firms must be able to demonstrate the use of a robust triage methodology whereby impacts categorized as harm, detriment or poor customer outcomes are prioritised for remediation. Other impacts, such as those related to service or journey improvements, can be then addressed later.

5. Enhanced Outcomes Monitoring and Management Information (MI)

A successful implementation plan will involve an evolution of how data and MI is used to test and monitor customer outcomes. The FCA has set out expectations that firms should be able to assess outcomes across end-to-end customer journeys, rather than simply focusing on procedural MI such as control effectiveness or lagging voice of the customer metrics such as complaints.

6. Policy and Sector Letter Traceability

Firms should be able to robustly demonstrate how each policy requirement has been considered throughout implementation. Many requirements may have already been met for all or some products and journeys, and this should be documented in a single repository of traceability. The Non-Handbook guidance should be used as an additional overlay on your traceability matrix to assure and test the application of the rules.

7. Day 2 Remediation and Capability Build

Most firms have a Day Two programme of some scope and scale in the planning. To demonstrate a compelling story to the regulator, firms should be signalling that – having achieved initial compliance – they are now mobilising more ambitious transformation plans to achieve customer centricity. This should include residual Day One review and remediation activities, ongoing evolution of outcomes monitoring and a continuous focus on delivering enhanced customer journeys with associated key controls. We provide further insight on focus areas for Day 2 programmes here.

8. Review of Closed Book Products and Services

Firms should not underestimate the complexities of implementing the Duty for off-sale products and services (set to come into scope from July 31, 2024) and should leverage the lessons learned and challenges identified during the on-sale review. As a first step, organisations should ensure their product inventory is comprehensive, including offerings accrued via acquisitions. We provide further insight on how firms should tackle the back book review here.